Irish people are highly taxed in some areas compared to EU norms, but pay relatively little elsewhere. As the debate rages on whether our tax base is still too narrow and over the future of issues such as the local property tax, new figures from the European Commission give a fascinating snapshot of what we pay and how it compares to the rest of the EU.

It shows the Irish tax structure is still heavily reliant on what are called direct taxes – those charged on the incomes of people and companies.

In many other areas, like property, the tax take here remains low. These trends frame the debate on what happens next with tax in Ireland, what you will pay and where you will pay it.

1. The overall picture

At first glance, Ireland seems like a low-tax economy, with overall tax revenues here equivalent to around 23 per cent of GDP, the lowest in the EU28. France (with a tax burden at 46.5 per cent of GDP) and Belgium (44.9 per cent) are top of the league. However, comparisons here are messed up by the old problem of our GDP figures being artificially inflated by the accounting activities of multinationals based in Ireland.

If we take the measures which the Central Statistics Office developed to factor out the multinational issue – adjusted gross national income, or GNI* – Irish tax comes in at around 37 per cent. This compares to an EU average tax take of 39 per cent of GDP. We are not comparing like for like here exactly, but it seems fair to conclude that the tax burden here is a bit below the EU average, though not as far as the unadjusted figures suggest.

Looking gloablly, the EU is a higher tax area so the tax burden here is roughly in line with international norms and higher than that in the United States and Australia.

We are not a high tax country. What we get back for the taxes and social insurance that we pay is, of course, another argument. Of which more below.

2. The top line trends

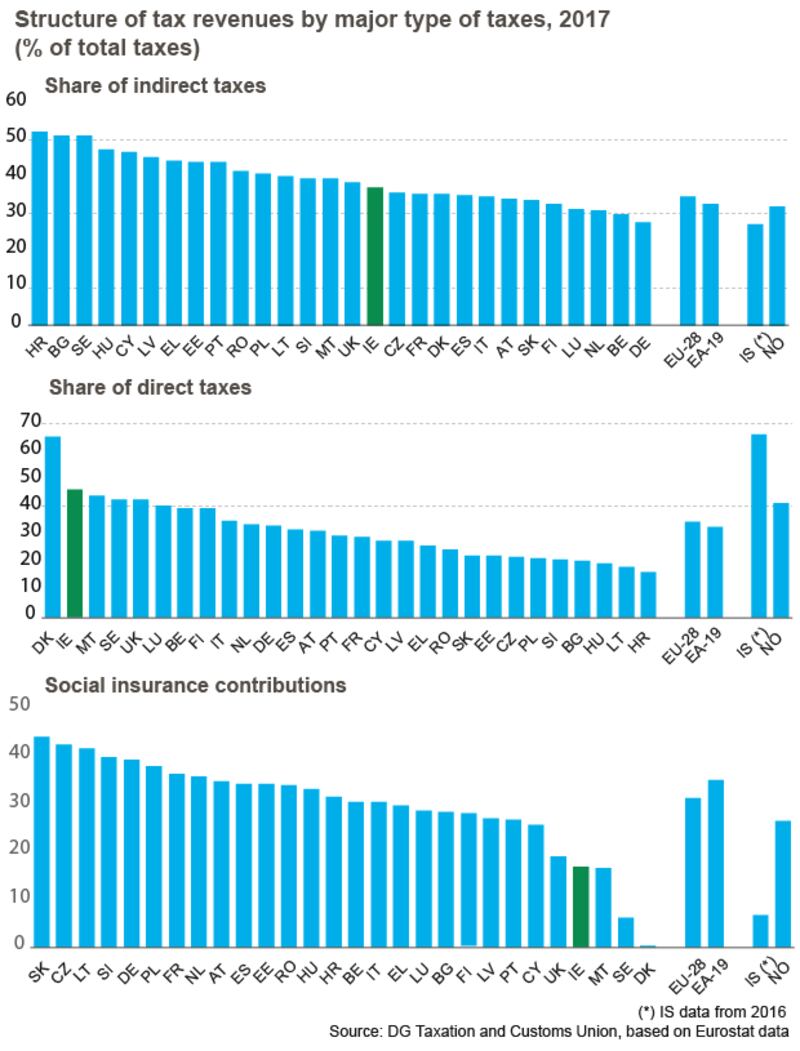

An interesting way to look at where tax comes from is to compare the three main types – direct tax, which is tax on personal income and company profits; indirect tax, such as VAT and excise; and social security contributions.

In all three cases the Irish position is notable. The share of direct taxes here, at 46.1 per cent of total revenue, is second only to Denmark’s remarkable 65.4 per cent. Our system relies heavily on income tax and corporation tax – and we might note that both are influenced by the economic cycle. We rely on the top 10 companies and a relatively small cohort of better off earners for a high percentage of our tax revenues.

On indirect tax, we are just above the norm – at 37 per cent compared to an average of just under 35 per cent. Excises on alcohol and tobacco are particularly high here. We pay for our sins in more ways than one. Our standard VAT rate, at 23 per cent, is just above the 21.5 per cent average.

Social security contributions here, however, are notably low at just under 17 per cent of total revenues, compared to the EU average of over 31 per cent. It can be difficult to compare as, in some countries. entitlements, notably in areas like health, are significantly better than in Ireland.

Many Irish families pay more via private health insurance than would be required if they lived elsewhere. However, the low social security take is a key factor in lowering the overall take on incomes here.

3. Tax on income

Tax and PRSI paid on personal income in Ireland are, on average, a bit lower lower than elsewhere in the EU. Tax on income makes up around 43 per cent of tax revenue here, versus an EU average of 50 per cent. The lower social insurance bill is a key part of the maths here.

The EU calculates the overall tax rate on labour here at around 33 per cent of earnings , compared to an average of around 36 per cent. We tend to pay relatively more in income tax and USC and less in social insurance (PRSI).

But the income tax take – compared to elsewhere – varies at different income levels. The latest EU report underlines that employees on relatively low incomes in Ireland pay low levels of tax compared to other member states.

For a single worker with average earnings, the tax “wedge” of income tax and PRSI is 10.6 per cent of earnings, compared to an EU average of 32.4 per cent. This is due to the structure of the Irish tax system and particularly the exemption of significant amounts of income from some taxes and charges. For example, people earning less than €13,000 pay no USC.

The latest data does not contain comparisons of the tax take on higher earners, though it does show the higher rate here – which it takes at 48 per cent to include USC but not PRSI – is well above the 39 per cent EU average. Other studies have shown that, at middle to higher income levels here, the tax take rises above international averages for many people.

As well as the relatively high top tax rate, the other key pinch point is that Irish earners become liable to that higher 40 per cent income tax rate at relatively low incomes levels by international standards. In terms of tax, the squeezed middle is a reality.

4. Tax on corporations and capital

The EU figures look at two separate sets of figures here. The first is tax on capital – for example tax levied on asset sales and on savings and investments held by individuals and companies. The overall rate in Ireland is calculated at 13.6 per cent versus an EU average of 30.8 per cent. It would be interesting to see a breakdown of this, splitting out households and companies. Yet clearly rates here are well below the highest in Europe, such as France (54 per cent) and Belgium (42 per cent).

The separate figures for tax on corporate income will only add to the debate about the taxes levied on big companies here. It shows a rate of 10 per cent tax rate on corporate income (excluding dividends) – below the 12.5 per cent statutory corporate tax rate, with only the Baltic states and Luxembourg coming in lower.

Our statutory corporate tax rate is also well below the 21.9 per cent EU average. Only Bulgaria and Hungary are lower than Ireland. We should note that, despite the low take on corporate incomes here relatively, corporate tax – which accounts for around one in every five euro – is relatively much more important here as a source of revenues.

5. Other taxes

A notable factor of the Irish tax system, compared to those elsewhere in Europe, is the low level of taxes collected in other areas. Talk of spreading the tax base did lead to the local property tax and we also have a carbon tax, but the flip side of relying on direct taxes for a large proportion of revenue is that the amounts collected in other areas are relatively small.

Environmental taxes in Ireland are the second lowest in the EU and energy taxes are also relatively low. Tax on property is also relatively low at just over 1 per cent of GDP, compared to 2.6 per cent of GDP in the EU (even allowing for the GDP distortion) and recurrent property taxes – like the local property charge here – are much higher in many other EU countries,. Total tax on property here accounts for 4.8 per cent of total tax revenue versus an EU average of 6.6 per cent

The policy pointers

There are a few important pointers for policy here.

- The reliance on direct taxes, and on a small number of big companies, does create a vulnerability in the event of a downturn, though perhaps not as serious as the reliance on property transaction taxes before the last crash.

- Widening the tax base has been slow and laborious. There is a big row over the extension of the local property tax, but it only collects some 1 per cent of revenue and there is no plan to increase this significantly. There is also a lot of sensitivity about increasing carbon tax – and the likelihood is that the net benefit to the exchequer could be small enough, initially at least. Politics is making it difficult to widen the base to new areas.

- Ireland's income tax base remains unusual. A low burden at low incomes is paid for by a squeeze higher up. Yet finding exchequer resources to, for example, increase the rate at which the higher rate kicks in is proving difficult. And wage rises mean income tax will take a bigger slice unless adjustments are made to bands and credits.

- Our corporate tax structure will remain under scrutiny in the international reform programme now underway and change looks inevitable, even if the shape of it is unclear. Ironically, while the level of tax on profits here is low, big companies book so much revenue here that this is an increasingly vital source of cash to our exchequer.

- We have an unusual social insurance system. A study on what people pay versus what they get and how this colmpares would be very useful. Talk of merging the USC and PRSI systems and extending benefits –– a European-type approach – was made by Fine Gael at the last election, but has run out of steam. An interdepartmental report on the issue had, finance minister Paschal Donohoe said in reply to a parliamentary question recently, shown that the issue was "a complex one which will take time to consider". Follow on decisions will be made "in due course" and will be made public "at the appropriate time". In other words, don't hold your breath.

This is the Eu report on tax trends if you want to read more.