:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/2PMUDOKJ7VD5DDIKLRQIAIKXLE.jpg)

:quality(70)/s3.amazonaws.com/arc-authors/irishtimes/49b5bd85-975f-4bb4-b7b2-a16ea7c1b3b2.png)

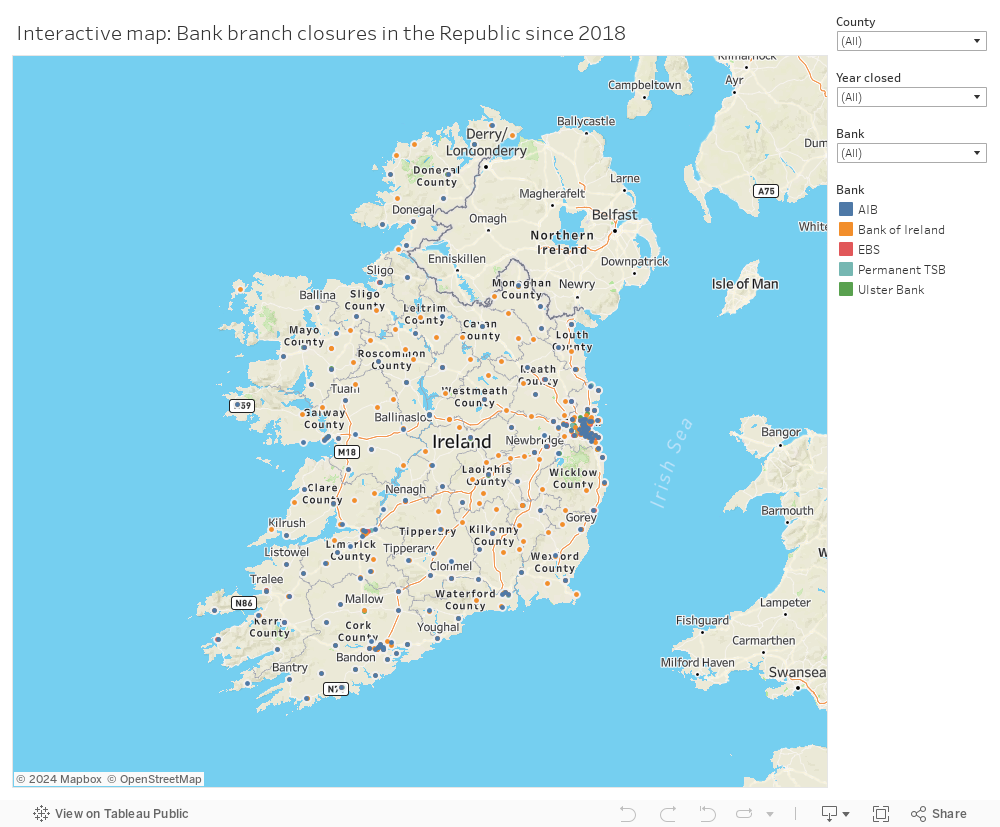

One of the stalwarts of Ireland’s banking sector has closed the doors of its branches for the last time.

Founded in Belfast some 187 years ago, Ulster Bank opened its first offices outside Ulster in Sligo and Ardee, Co Louth in 1860, followed by a Dublin branch in 1862.

It subsequently became one of the largest banking entities in the Republic.

Now the bank is gone. The final closure from Ulster Bank comes hot on the heels of the departure of Belgian bank KBC Bank, which closed most of its branches back in March. It means that the list of options for everyday banking has shrunk yet again.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/6BDEAESQEJH4BHNFRSVZH3W4TM.png)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/SJH7MUGACCC3EMUPM7BS4YQFFY.jpg)

:quality(70):focal(738x308:748x318)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/MFTGHTWVFYVACWQA7U4UJQEFKY.jpg)

But, unlike with deposits perhaps, there are a growing number of banks and emoney providers providing payment services in Ireland. However, the offerings do differ from provider to provider, and due caution is needed before making a switch to ensure that a) you actually end up saving money; and b) you get the banking service you need.

‘Pillar’ banks

With the departure of Ulster and KBC, just three traditional or “pillar” banks remain in Ireland. First up is AIB, which has a quarterly fee of €4.50 (free for AIB mortgage account holders) as well as a raft of additional fees, which mean typical charges work out at about €7.15 a month or €85.80 a year, according to estimates from Bonkers.ie.

These fees include 35 cent for ATM withdrawals, 20 cent for an online or phone transaction and 20 cent for a debit card purchase.

This makes the bank one of the more expensive on the market unless you have a mortgage with them – although, as you’d expect, the bank does offer everything one might expect from a current account.

You also have the newer bells and whistles, such as Google Pay etc and a decent app, plus access to a chequebook as well as an extensive branch network, overdrafts, personal loans, and a telephone/in person support service.

Bank of Ireland also offers a full service current account, although some might grumble about its mobile banking app when compared with other offerings.

Again, you’ll have to pay up-front for it with a flat fee of €6 a month, although this does mean there are no fees on daily transactions. As with AIB, you can get an overdraft, chequebook or personal loan, as well as newer services such as Apple Pay etc. You also have access to a branch network.

Like Bank of Ireland, Permanent TSB (PTSB) has a relatively steep quarterly account maintenance fee of €18 (which works out at €6 a month or €72 a year) but no day-to-day transaction charges.

What sets it apart, however, is that it offers cash back on a range of transactions, although this is capped at €5 a month. For example, you get 10 cent back each time you use your debit card; so use it 50 times and your net charges will fall to €1 a month.

In addition, you can get 5 per cent cash back on a variety of bills from service providers including Sky and Circle K, when you pay via direct debit.

All this means that the monthly fee for the account, based on typical usage is just €2, according to Bonkers.ie.

AIB’s subsidiary EBS is the only pillar bank that still offers “free” banking as there are no changes on its Money Manager account. If you can live with not having a mobile banking app (though you will have online banking) or an overdraft facility or chequebook, this could be a good option for you, as you get a good product at a low cost.

Bonus: Depending on your age, you might find everything you need with these older, established players, as they offer free banking to the older cohort, starting at 66. And, while banks have stepped up bank closures in recent years, it is still possible to find one in your area should you need to speak with someone or access services.

Fintechs

With traditional bank entrants all but gone, the only new players on the Irish market in recent years have been from the so-called “neo” bank sector, with challenger banks embracing technology to cut costs and reach a wider group of customers without the need to have a physical presence.

In Ireland, the biggest fintech player remains Revolut. More than a million Irish people now have a Revolut account but many use it primarily for sending or receiving payments.

However, the company is now deemed to offer a full service current account offering, after it was regulated as a bank in Lithuania. This means that deposits from Irish customers are covered under that country’s €100,000 deposit protection scheme.

Irish account holders now also have an Irish Iban – before this a Lithuanian international bank account number was used. While this shouldn’t have been an issue, in practice it was, because some utility companies and others wouldn’t accept payments from a non-Irish Iban. With an Irish Iban, this should no longer be an issue.

There is also the option to upgrade for better features, with plans starting at €2.99 a month and rising to €13.99 for the provider’s metal account, which offers cash-back of 0.1 per cent a month, up to a maximum of €13.99.

If you sign up for a standard account, you won’t be hit with any monthly fees; but you will have to rely on web chat for support if things go wrong.

As with Revolut, a standard account with German bank N26 is also free. However, you don’t get a physical debit card with this account so it is limited. You’ll have to upgrade to the bank’s Smart account, which costs €4.90 a month (€58.80 a year) to get one, or pay a fee of €10.

Moreover, there is no telephone support (just online support) on the standard account. To access phone support, you’ll need to pay, from €4.90 a month for a Smart account, and €16.90 for a Metal. These options come with phone support, while the latter also comes with travel insurance.

Bear in mind however, that the bank is currently closed to new customers in Ireland. A spokeswoman says that due to “overwhelming demand” for its simple product, it has had to limit availability of the product. If you apply, you’ll go on a waiting list.

“Our goal is to offer all prospective customers the ability to sign up for an N26 account of their choice as soon as possible,” she says.

Dutch online bank Bunq entered the Irish market last year, offering three current account options, starting at €2.99 a month for its “Easy Bank” option, increasing to €17.99 for its Easy Green option.

Deposits on your Bunq account are automatically protected up to €100,000 by the Dutch Deposit Guarantee Scheme. And it’s an important point to note, because Bunq is the only bank currently offering customers interest on deposits.

You can earn 1.56 per cent on deposits of up to €100,000, and you’re allowed withdraw from the account, so it’s by far the best instant access account on the market.

Finally, Money Jar says it’s the first Irish-owned neo/fintech payment provider. An emoney account, deposits with Money Jar are not protected by a deposit guarantee scheme, but your money is held by a Tier 1 state owned Irish bank.

Money Jar customers get an Irish Iban, and the account offers incentives such as unlimited money jars that can be shared with friends, to help you stay on top of personal spending and to save.

Bonus: The fintechs offer some of the cheapest current account offerings on the market – and you can even earn interest with one of them, as Bunq pays 1.56 per cent on deposits.

Post office

Another option is through your local post office. With An Post Money, you’ll have access to An Post’s branch network of more than 900 outlets.

You’ll also get the latest tools, such as Google and Apple Pay, as well as app banking – but no chequebook or overdraft.

However it is expensive; Bonkers.ie estimates that your monthly costs will typically work out at about €6.80, or €81.60 a year, based on the monthly €5 fee, plus three ATM withdrawals at 60 cent each.

Bonus: Last year a new smart budgeting tool, Money Manager, was launched with the current account. It allows you to set budgets, and track your spending. Other initiatives to help you save include offering “jars”, or mini savings accounts to save for different goals, as well as rounding up your debit purchases and allocating more money to your savings account.

Credit unions

You can also consider your local credit union for your everyday banking needs.

More than 70 credit unions across 220 locations currently offer a current account service, according to the Irish League of Credit Unions (ILCU).

Credit unions which offer the service include Access Credit Union in West Cork, Claddagh Credit Union in Galway, and Core Credit Union in south Dublin.

You’ll pay a monthly fee of €4 for your current account (€48 a year), which offers a full service current account offering, with app banking, new innovations such as Google or Apple pay, as well as regular fixtures of your current account such as access to an overdraft.

When it comes to savings however, opting for a credit union may be a bit trickier, as many still have limits in place on the amount of deposits they’ll accept, despite the changing interest rate environment. At St Francis Credit Union in Ennis, Co Clare, for example, the savings limit is €20,000.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/6I7JZS7NGRBVLADOPZD35KKEO4.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/BAIYZJTDJ2UFIS63YW6LKXOZWE.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/RYR775WNEKM2CS76SR52N42TIY.JPG)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/JVRVDZYCYIJA46OBIUDID5FZRE.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/5HDKWUOYHJEAPO2SZ4TTTNAKBU.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/UVGJZFCBWH4WRCTUFLJNJXWEOE.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/WIDSALIJYCBCARRW6NQHRDORVY.jpg)

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/5SZ3UCJGBQIIGOVOMIAKGDFGII.jpg)