If you have cash on deposit at the moment, you’re losing money. And not just a bit, but a lot. With inflation still at a heady 7.7 per cent in March, and the typical saver earning significantly less than 1 per cent on their money, the real value, or inflation adjusted value, of Irish savers’ money continues to fall.

Despite interest rates jumping ahead to try to put a brake on soaring prices, there is little indication that deposit rates will offer much relief in the short term.

European Central Bank interest rates have surged from zero last July to 3.5 per cent as of end-March, with yet more hikes expected. Typically, one would expect this to translate to on-demand deposit rates of somewhere around 2 per cent – but rates continue to languish much lower.

Ireland is not alone in underpaying savers. Online deposit broker Raisin, which is backed by Goldman Sachs and Deutsche Bank among others, recently accused German banks of short-changing savers with low interest rates, with its data showing two-thirds of sparkassen not paying any interest on overnight deposits.

READ MORE

Banks have started to edge up their rates, but the increase has largely been minimal thus far

It is particularly galling for Irish consumers given that not so long ago, they endured some of the highest interest rates on mortgages across the euro zone, at a time when low ECB rates pushed 20-year home loan rates to as low as less than 2 per cent in countries like France.

Banks benefit

Of course, low deposit rates suit the banks, at a time when competition is diminished and savings remain buoyant. Latest figures show that retail deposits stood at €315 billion in December, up from €286 billion at the start of the year. And much of this is sitting in the pillar banks’ coffers.

AIB’s customer deposits, for example, rose to €102 billion as of end-2022, up from €93 billion a year earlier, while at Bank of Ireland deposits rose to €99 billion, up from €93 billion a year earlier.

[ Why are savers being held to ransom by Ireland’s banks?Opens in new window ]

There are a number of reasons why banks have only moved very slowly to improve rates. For one, the dynamic of offering better deposit rates to attract savers’ money which can then be lent out again doesn’t exist. “Deposits in the system significantly exceed the loans in the system at this point,” says Diarmaid Sheridan, financials analyst with Davy.

For another, Irish banks have been slower than others to increase mortgage rates on the back of ECB hikes, which means Irish borrowers are doing better than others in this respect – but at the expense of savers.

And, of course the lack of competition is a key issue.

“Right now, the dynamics would suggest that none of the banks need to go out and aggressively price [deposits],” says Sheridan.

Such high levels of deposits have become a readily available source of funding for the banks. Consider this statement from the AIB’s annual report, published in March of this year:

“Customer deposits represent the largest source of funding for the group with the core retail franchises and accompanying deposit base in both Ireland and the UK providing a stable and reasonably predictable source of funds.”

What it omitted to say, of course, is that it’s also a very cheap source of funds. The best rate currently offered savers by the bank is a miserly 0.5 per cent – far less than both the ECB lending rate of 3.5 per cent or even the 3 per cent rates it pays AIB and others that deposit money with the Frankfurt central bank.

The dynamics would suggest that none of the banks need to go out and aggressively price deposits

While higher rates may be costing the banks in other areas, paying so little on deposits must have a beneficial impact on the bank’s bottom line. Back in 2012, for example – a time when deposit rates were still attractive at about 3 per cent – AIB reported interest expense on customer accounts of some €1.3 billion. Fast forward to 2022, and it had plummeted to just €46 million, according to AIB’s latest annual report.

Banks have started to edge up their rates, but the increase has largely been minimal thus far.

In February, for example, AIB announced a number of increases. Regular savers saw their return jump from just 0.1 per cent to 1 per cent on savings of up to €1,000 a month. Once a year passes, however, the rate drops back to just 0.1 per cent.

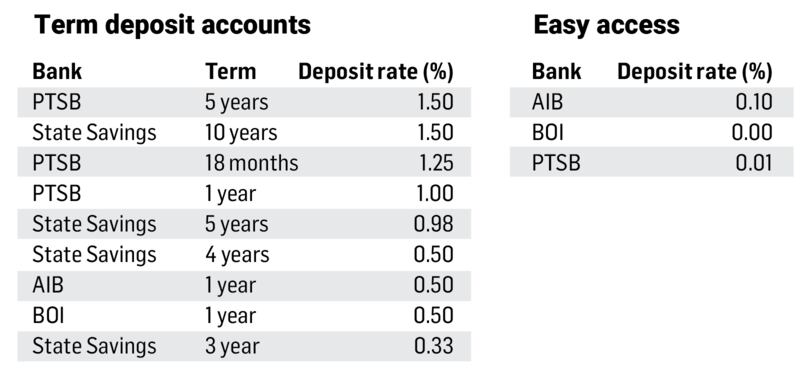

Bank of Ireland and Permanent TSB have also increased rates, but in a world where there are now just three banks offering deposits (as well as the AIB-owned EBS), competitive pressures have been muted. As our table shows, rates are still almost at zero for instant access accounts, while over a fixed term, the best rate available is 1.5 per cent a year with Permanent TSB or State Savings – but you have to lock your money away for five or 10 years.

Euro zone rates

Ultimately, it means that Irish customers are finding themselves at odds with euro zone norms just as they did until recently on mortgage rates.

According to the European Central Bank, the typical rate on household term deposits rose to 1.64 per cent in January across the euro zone; figures from the Central Bank show the equivalent Irish rate was just 0.71 per cent, which means it is less than half the euro zone average.

In the Netherlands, you can earn 2.75 per cent on a one-year fixed rate with Turkish bank Yapi Kredi.

In the UK, where the Bank of England rate now stands at 4.25 per cent – three-quarters of a point higher than the euro zone – you can earn 3.22 per cent on an instant access account with Sainsbury’s Bank, or 4.05 per cent on deposits of up to £5 million on a one-year fixed rate with Tesco Bank.

Meanwhile in France, savers got a welcome boost in January when it was announced that the rate on offer for the Livret A, which offers savers guaranteed and tax-free returns on rates set by the Ministry for Finance, would increase from 2 per cent to 3 per cent. Some 55 million French people have such an account, latest figures show, with the deposits used to fund social housing.

Deposits in the system significantly exceed the loans in the system at this point

It’s a significantly more attractive offering than that available in a similar scheme in Ireland – State Savings. While the NTMA has increased the rates on State Savings recently, they are still far below euro zone norms. Also guaranteed and tax-free, savers can now earn an annual rate (AER) of 0.98 per cent on five-year savings certificates for a total return of 5 per cent, or on instalment savings for a total return of 5.5 per cent. The best return is on the 10-year solidarity bond, which offers 1.5 per cent over a decade for a total return of 16 per cent.

It means that an Irish person could earn €500 on savings of €10,000 over five years. By contrast, in France, you could earn €1,590 – a substantial difference.

Savings in a Livret A can be withdrawn at any point, and your money isn’t locked in – unlike with State Savings. However, a more modest upper limit, of €22,950 applies to the amount you can deposit, compared with €120,000 per State Savings product.

It’s also worth noting that, back in March, the NTMA paid institutional investors its highest interest rate in nine years, when it sold €800 million in long-term bonds at a rate, or yield, of 3.37 per cent. It’s only Irish savers who have to settle for less, it would seem.

Regular savings

AIB Northern Ireland: 3.5%

AIB Ireland: 1%

Term deposits (one year)

Banco Português de Gestão, Portugal: 3.15%

Bank of Ireland: 0.5%

Tax-free, guaranteed savings

Livret A, France: 3% AER

State Savings, Ireland: 0.33% AER*

* There is no equivalent instant access State Savings account, so the AER given is for the lowest term, the three-year product