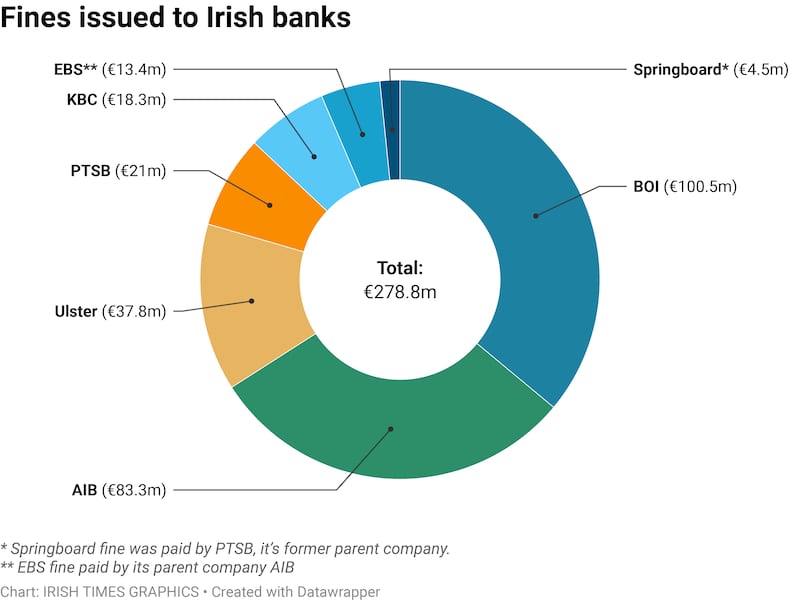

The Central Bank, which fined Bank of Ireland a record €100.5 million on Thursday for its role in the tracker-mortgage scandal, pinpointed late 2017 as a turning point for the group’s attitude towards customers affected by the tracker mortgage crisis.

It was at a time when Francesca McDonagh had just taken over as chief executive. Not that the London-born banker had much choice, taking on the job just as political and public uproar over the industrywide overcharging scandal, then dragging on for almost a decade, was screeching towards a crescendo.

Between October 2008 – when Irish lenders stopped offering cheap mortgages tracking the European Central Bank’s (ECB) main rate as their own funding costs spiralled out of control – and November 2017, Bank of Ireland doggedly interpreted “unclear and ambiguous” mortgage documents in its own favour to avoid allowing customers to avail of tracker rates after a period on a fixed rate.

During the nine-year period, the bank failed to warn customers that they would lose their tracker mortgage rights if they moved to a fixed rate or if they broke early from a fixed-rate period, the Central Bank said. It also omitted letting borrowers already in financial trouble know that they would lose a future tracker mortgage entitlement when signing up to a forbearance arrangement.

READ MORE

What was even more egregious was the finding that Bank of Ireland’s board consistently made decisions on whether certain groups were affected by overcharging or not “in the absence of key material information to enable it to make an informed decision” until late 2017. Were non-executive directors deliberately kept in the dark? Or did they not do their job and ask the right questions?

While Bank of Ireland admitted thousands of additional cases for compensation in late 2017, it would take another five years for Central Bank officials to be able to finalise its enforcement investigation into the State’s largest bank by assets. Even until a few months ago, Bank of Ireland was still finding affected customers – with the admission in June of six cases that had previously been excluded from redress and compensation. It brought the total to 15,910.

With McDonagh having moved on earlier this month to take on a senior role at embattled Swiss lender Credit Suisse, it fell to interim chief executive Gavin Kelly to issue the obligatory grovelling apology.

“We have learned the hard lessons, and have taken steps to ensure we are a more customer-focused bank today,” he said. “This work continues. Rebuilding the confidence of both our customers and the wider society we serve will take time, but we are committed to that journey.”

Tell that to one of the previous owners of 50 properties – half of which were family homes – that were lost by Bank of Ireland customers as overcharging tipped them over the financial edge. No amount of financial compensation can undo the suffering inflicted on those – or the individuals behind a wider 327 houses lost across the industry.

The Irish Banking Culture Board (IBCB), set up by the sector four years ago in the wake of the debacle, came out quickly on Thursday to say the last of seven tracker enforcement cases to a close must act as “a bookend to the unacceptable behaviour and culture within banking”.

Chaired by former Court of Appeal judge Mr Justice John Hedigan, the IBCB has promised to hold a round-table event in the coming months, bringing affected customers, regulators and banking executives together to “reflect on the core behavioural and cultural issues we consider must lie at the heart of the post-tracker banking industry in Ireland”. Do we really need another talking shop?

The Central Bank, which also took its time in setting up an industrywide investigation into tracker issues in 2015, would also like to believe that things have already changed.

Consumer protection

Derville Rowland, a deputy governor of the Central Bank in charge of consumer and investor protection, highlighted that the regulator’s consumer protection code has been strengthened since the financial crisis and expectations of lenders are “clearer than before”.

Certainly, the regulator has shown that it has become a credible enforcer of late, willing to impose previously unthinkable fines on banks for their actions in the tracker debacle. The then-record €21 million levied against Permanent TSB 2½ years ago has since been dwarfed by penalties imposed on Ulster Bank, AIB and its EBS unit and, now, the first €100 million-plus fine.

But these will not be enough to restore public trust in banks – especially when bank customers know all too well that they will ultimately carry the cost.

Consumers now need to see individuals involved in the scores of regulatory breaches carried out by banks in relation to tracker loans held to account. It’s almost 11 months since the regulator decided to subject an initial individual to an inquiry, with no apparent progress on the case to date.

Seána Cunningham, the Central Bank’s director of enforcement, insisted to reporters on Thursday that “individual accountability is an area of focus” for her team, and that “we will take action where we believe it is merited and appropriate”.

As much as Thursday’s sanctioning of Bank of Ireland is being billed as a milestone day, the saga is far from over.

Even now, almost a decade and a half after the tracker controversy began, we still have lenders – namely Ulster Bank and Permanent TSB – fighting through the courts decisions by the Financial Services and Pensions Ombudsman to include certain customers for redress, after being disregarded in the industrywide examination overseen by the Central Bank.