Ten years ago this month the clouds were building, but we had little clue of the extent of the economic storm that lay ahead. Stock markets were creaking, there were signs of strain in international banking, and the Irish housing market had already come off the boil. After the most extraordinary period of Irish expansion it was clear the cycle had turned. But there was no hint, in January 2008, of the economic tsunami that was approaching.

Had you told anyone what lay ahead – the bust and the bailout – they would surely not have believed you. And five years later, in January 2013, had you predicted the growth that lay ahead, you would have got a similar reaction.

It is tempting but not quite correct to call it a roller coaster. Roller coasters start and finish at the same place. On the face of it many of our key economic figures are now back at or close to prebust levels, most importantly the money people have to spend and the number of people at work. But look more closely and much has changed. In some areas the scars of recession remain: about one in 10 households is in negative equity, more than 8 per cent of the population live in consistent poverty and 7 per cent of mortgages are still more than three months in arrears. All these indicators have improved significantly, but they remain stubbornly high. Above all else, the housing crisis shows how the emergency-era cuts are still taking a toll.

Tents and sleeping bags

Christmas highlighted the dichotomy in economic fortunes. Tills were ringing, Retail Ireland said sales would approach the 2007 record, and many restaurants were heaving. But tents and sleeping bags remain common in our cities and towns, there were are queues for hostels and the Capuchin centre in Dublin said the number of food parcels it gave out was up threefold compared with five years ago.

On the flip side, the boom in jobs and investment has created new opportunities and brought pressures of congestion in Dublin and the other major cities. The benefits of recovery have spread across the country, but structural trends, such as online shopping, have left many country main streets in poor shape.

The economic boom is back – this time the same only different. And the Government and policymakers face the big question. Can we stop ourselves moving into another cycle of boom and bust? Are Ministers serious when they say they want to move the economy into steady and sustainable growth? And can they accelerate progress in dealing with the remaining scars of the crisis, notably homelessness?

We just don’t do steady, boring 3 per cent growth. Over the past 20 years annual economic growth here has been within what might be called a normal, sustainable range of 2 to 4 per cent on only three occasions.

The year ahead will be a defining one. We have reached our EU borrowing benchmark. Some €3 billion or more might be available for tax cuts and spending increases in the budget. But the right thing to do may well be not to spend it all and to squirrel some away for when the downturn hits.

It will also be a vital year in addressing the other two issues likely to define the Government’s term in relation to the economy, one being a legacy of the bust – housing – and the other, of course, being Brexit. Politics is all about choices. During the bust the Government seemed to be backed into a corner. But, as Leo Varadkar and Paschal Donohoe will learn, being spoilt for choice has its problems too.

Gathering storm clouds

In January 2008 it was all about the United States economy. Storm clouds were gathering, emerging from complex financial instruments that were , in effect, a kind of badly constructed Ponzi scheme based on lending to less well-off US homeowners in what was called the subprime housing market.

The US central bank – the Federal Reserve – cut interest rates twice that month, slashing its base rate from 4.25 per cent to 3 per cent. President George W Bush announced an emergency budget, pumping almost $150 billion into the economy. One thing you can say for the Americans is that when this all hit they did not hang around.

In hindsight we can see that the US economy was then just entering recession, brought on by the spreading impact of a failure in its financial system, and that the slide was about to accelerate.

Looking back at The Irish Times a decade ago, there is a clear sense that trouble is on the way but few hints of how dramatic it will be. The pieces of the puzzle were all starting to fall into place, but nobody could see the full picture.

Internationally, signs of strain were emerging. Many people date the key moment to August 9th, 2007, when BNP Paribas froze three investment funds because, it said, it had no way of valuing the complex financial structures involved, based on US subprime loans. In September Northern Rock building society had been bailed out by the British taxpayer.

But here, we were told, it was different. Irish banks had little exposure to these complex financial instruments, it was said. The problem was that they were exposed to the ticking time bomb of the Irish property market.

By January 2008 housebuilding had started to slow and house prices were off their peak. Unemployment was on the rise, fuelled largely by construction lay-offs. But the most pessimistic forecast I could find in reports that month was from a stockbroker who predicted the economy was to grow by 2.3 per cent that year and bounce back the next. In the event GNP fell by more than 2 per cent in 2008 and collapsed by more than 6 per cent in 2009.

In an Irish Times article in December 2006 Prof Morgan Kelly of University College Dublin had warned of the vulnerability of the property market. The following September he had cautioned about the risks banks faced from property lending. But the Government and the Central Bank continued to insist that, although we might face some challenges, all was well.

Ireland was "well equipped" to deal with any international downturn, policy was " well thought out and sound", and we should not over-react to short-term stock-market moves, according to Bertie Ahern, who was speaking, as taoiseach, in January 2008. The banking sector was "stable and well placed to withstand market turbulence", according to the governor of the Central Bank of Ireland, John Hurley.

After January 2008 an eerie calm prevailed, but only for a couple of months. In March the American investment bank Bear Stearns had to be bailed out and Anglo Irish Bank shares wobbled. In September Lehman Brothers went bust and the financial world had a heart attack. A few weeks later came the bank guarantee.

We often forget how slowly the story then unfolded. One day stands out, March 30th, 2010, when, as minister for finance, Brian Lenihan told the Dáil that the bailout of Anglo Irish Bank alone was likely to cost more than €20 billion. That was the moment we disappeared off the top of the roller coaster and headed for the inevitable bailout.

As the reality was laid bare over the following couple of years – the banks were guaranteed and Ireland collapsed into a bailout – there was to be a fracturing of trust between politicians, the administration and the people, one whose consequences will be felt for many years to come.

Five years of recovery

We exited the bailout at the end of 2013, with the economy then growing faster than most had anticipated. It hasn’t stopped since. A decade after the crash there is no doubt that the Irish economy bounced off the floor more quickly than anyone expected. The 10 years since 2008 can be divided in half: five years of bust followed by five of recovery.

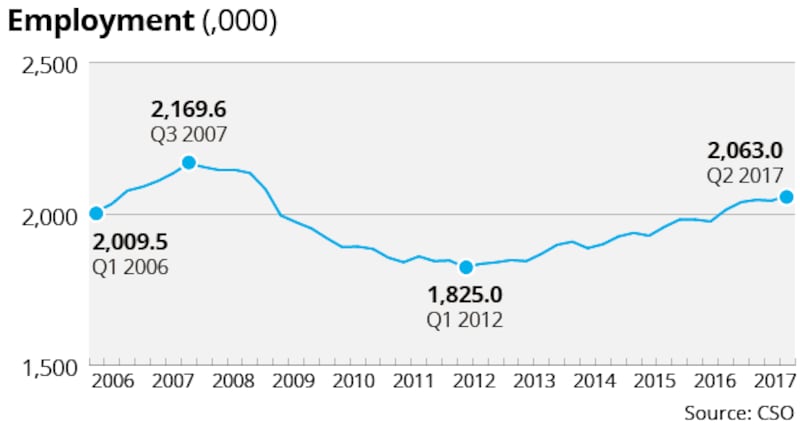

The key indicator has been employment, up from just over 1.8 million, at its lowest point, in 2012, to well over 2.1 million now, closing fast on its all-time peak, of 2.2 million, in 2007. Economic growth, even allowing for the distorting impact of multinational activity, has been robust. And the exchequer is close to balancing its books.

All this is being felt in people’s pockets. The average disposable income collapsed by 14 per cent between 2008 and 2012, from €20,681 to €17,702, and recovered to €20,597 by 2016. Given income and job growth in 2017, we will by now have exceeded the 2007 peak.

The averages hide a multitude, of course. A distinct group is now living under the cosh of record rents, for example, which cuts their discretionary spending. But rising incomes and increasing employment are the clearest signs of the recovery improving people’s lives.

The worst of our problems, the housing crisis, dates back directly to the financial crisis. Work started on more than 75,000 new homes each year from 2006 to 2008, but by 2011-13 that figure had collapsed to between 4,000 and 5,000 a year. The construction industry was decimated: builders went bust or into Nama, banks had no cash to lend and were under pressure to shrink their loan books, and State investment in housing was slashed.

The lack of housing supply is at the root of much of the homelessness crisis, of soaring rents and of rising prices that have pushed homes out of the reach of many young buyers. Dangerous feedback loops have led to high rents pushing some into homelessness and ensuring that others cannot afford to save to buy somewhere to live. Housing starts are at about 15,000, but there is much still to do. It is not the credit-driven bubble of the mid-2000s but a drastic, damaging housing squeeze.

Although the headlines reflect the social crisis it has caused, housing is also now a constraint on our economic growth. Certainly in Dublin it is part of a story of infrastructure investment, which was slashed during the recession. Not only in housing but also in crucial commuting infrastructure and an orbital ring road – the M50 – already operating beyond its limits, Dublin is bursting at the seams.

In terms of attracting companies to invest here, this is now a crunch issue. Modern companies rely on talent, and talent needs somewhere to live affordably, a way to get to work and a chance of a decent lifestyle. Dublin is struggling to provide these.

Pick where to spend

The Government faces the twin challenges of dealing with the legacy of the bust and the challenges of the recovery. The threat of Brexit, which could yet deliver a hard shock in 2019 were the UK to crash out without a deal, remains.

The big lesson from the crisis is that it is too late to act when the bubble is inflated. Things could have been done in January 2008 to soften the blow, but by then the damage was done and the fuse was lit. We needed to act four or five years earlier.

This time it is different, but that doesn’t mean it’s not still dangerous. We don’t have a credit-driven housing bubble, but we are still at risk of watching prices shoot above sustainable levels. The public finances are sounder but remain vulnerable to volatile corporate-tax receipts. Inflation is low, but prices still make Ireland an expensive place to live, hitting people’s lives and threatening competitiveness.

If Brexit does not end too badly we could be looking at a few more years of decent growth, albeit at a slower rate as the economy starts to approach capacity. We could have a chance to futureproof our public finances and start to make headway in the housing crisis.

History won’t repeat itself exactly. The crash of 2008 was, let’s hope, an event we will never see the like of again in our lifetimes.

But, looking out over the next few years, the world will change. The UK will leave the EU, interest rates will start to rise from rock bottom, and the favourable backdrop of strong growth across the industrialised world will, sooner or later, be upset. The challenge is to be prudent, to pick where to spend, to get value for money and to accept that the taxes we pay are not going to fall much from current levels.

Another challenge is to do the hard work and divert resources to address the enduring human cost of the slump.

If, instead, the political narrative over the next year is dominated by talk of tax cuts and politically driven spending increases, then you will have to conclude we deserve what is coming to us when the economic cycle turns, as it always does sooner or later.