An iceberg lurking. Or a ticking timebomb? Ireland’s national debt, a sizeable €240 billion, surged during the pandemic, and Government plans to reduce the debt burden gradually in calmer times are now under threat from the war in Ukraine. When the European Central Bank meets on July 21st, an increase in its official interest rates is now certain, but borrowing costs for the State have already risen sharply in anticipation of this. The days of “money for nothing” – or at least at zero interest rates – are well and truly over. But what does this mean for Ireland’s national debt and for the framing of Budget 2023?

Ireland has bitter experience of what happens when the public finances go out of control, as happened after the financial crash in 2008, eventually leading to the State being bailed out in 2010. There are no similar warning lights at the moment. But the scale of Ireland’s debt means two things.

First, it restrains the Government’s room for manoeuvre in the budget for 2023 and the years ahead.

Second, it is an exposure if international economic conditions take a big turn for the worse, hitting growth and leading investors to be more cautious in who they lend to. Bodies such as the Irish Fiscal Advisory Council (IFAC), the budget watchdog, warn that reducing this risk needs to be a key goal of policy, particularly as Ireland is increasingly reliant on unpredictable corporate tax revenues. With talk swirling in markets of new pressures on European sovereign debt markets, nervous months may lie ahead and Ireland does not want to be in the firing line.

READ MORE

Market confidence looks set to be tested in the months ahead. Investors are again getting nervous and Italian debt, in particular, is under a bit of pressure

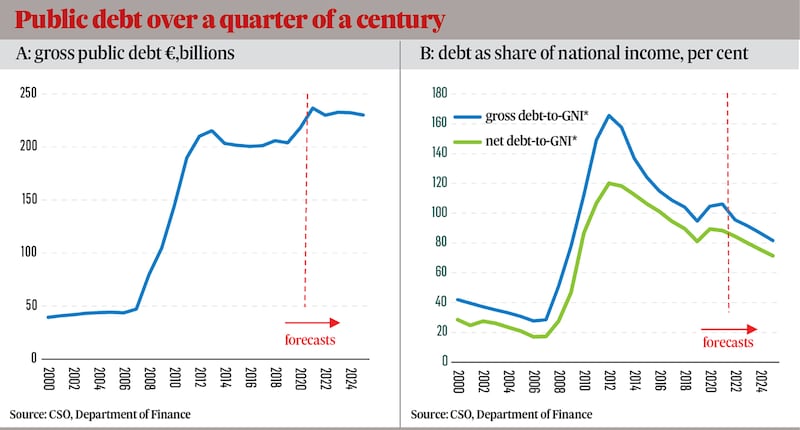

Ireland’s national debt has had two big jumps in scale in recent years. The first happened during the financial crisis when a big hole in the exchequer finances and the need to bail out the banks led to a massive jump in borrowing – first from the markets and then via the bailout from the EU and IMF. The size of the national debt rose from less than €50 billion before the financial crash in 2006/7 to a peak of €215 billion in 2013. The national debt then stabilised at a cash level of around €200 billion, with economic growth and low interest rates meaning the burden was gradually reducing.

Then emergency Covid-19 borrowings sent it soaring again to about €240 billion – though the ability of the National Treasury Management Agency (NTMA) to borrow new debt and refinance the huge financial crash borrowings at zero interest rates meant annual repayments have actually fallen. The plan was to stabilise the cash amount of the debt over the next few years, reducing its burden as the economy grew. Then the war in Ukraine hit.

The increase in the borrowing costs on new State debt since the start of the year has been remarkable. The cost of new 10-year borrowing for the Irish State has risen from just over zero at the start of the year to as high as 2.5 per cent, before easing to just over 2 per cent now. This is in line with increases elsewhere and is still cheap by historical standards – borrowing costs rose to 15 per cent before the 2010 bailout. But there is a sense that the world has changed – that we may be entering what Minister for Finance Paschal Donohoe referred to as a new economic era, with more frequent and severe shocks, lower growth and higher inflation.

How far will a €6.7 billion budget package get us?

UCC economics lecturer Seamus Coffey and Tom McDonnell Co-Director of the Nevin Economic Research Institute (NERI) join Cliff Taylor to discuss the Summer Economic Statement which was published this week and the €6.7 billion budget package poised to tackle the spiralling cost-of-living crisis.

In this context, a high national debt means two things. First, it will constrain policy in the years ahead. Ireland’s debt is at the higher end of the EU league table. Debt as a percentage of the domestic economy is about 106 per cent, compared to an EU average of 79 per cent. Ireland cannot afford to move too far out of line with deficit and debt levels elsewhere.

The second exposure is if there is a big hit to economic growth – most likely from an international recession, perhaps sparked by ongoing fallout from the war. A gas crisis, threatening supplies and sending prices sharply higher, is the most obvious catalyst. By hitting economic growth, this would also hit tax revenues. If inflation was still high, then interest rates might still be on the rise. A hit to profits of the big US multinationals could reduce tax revenues here – their share prices have already slid sharply. The Central Bank and Department of Finance are the latest to warn of the risks of relying on this revenue, with the bank saying that up to €8 billion of annual revenues – more than half of the 2021 total – could be unsustainable.

The dynamics of national debt mean that the debt burden falls for as long as the economic growth rate is above the debt interest rate. So a recession could turn around positive trends. The vast bulk of outstanding debt is at a fixed interest rate, so higher borrowing costs come into play for new borrowings, or when old debt must be rolled over.

Market confidence looks set to be tested in the months ahead. Investors are again getting nervous and Italian debt, in particular, is under a bit of pressure. As the comfort blanket of fresh ECB buying of Government bonds in the market – part of the pandemic supports – ends, these gaps between German and peripheral interest rates will be tested further, particularly if Europe lurches into a recession. The key issue for Ireland is to retain its place as a middle-ranking, or mid-tier, country; we will never have German borrowing rates, but we can hope to remain aligned with countries such as France and Belgium.

”Ireland is in mid-tier land instead of PIIGS land,” according to a dealer with many years of bond market experience, referring to the acronym for the group of countries who came under pressure during the financial crisis – Portugal, Italy, Ireland, Greece and Spain. “If trouble hits again we need to make sure there is only one ‘i’ in PIGS,” he added.

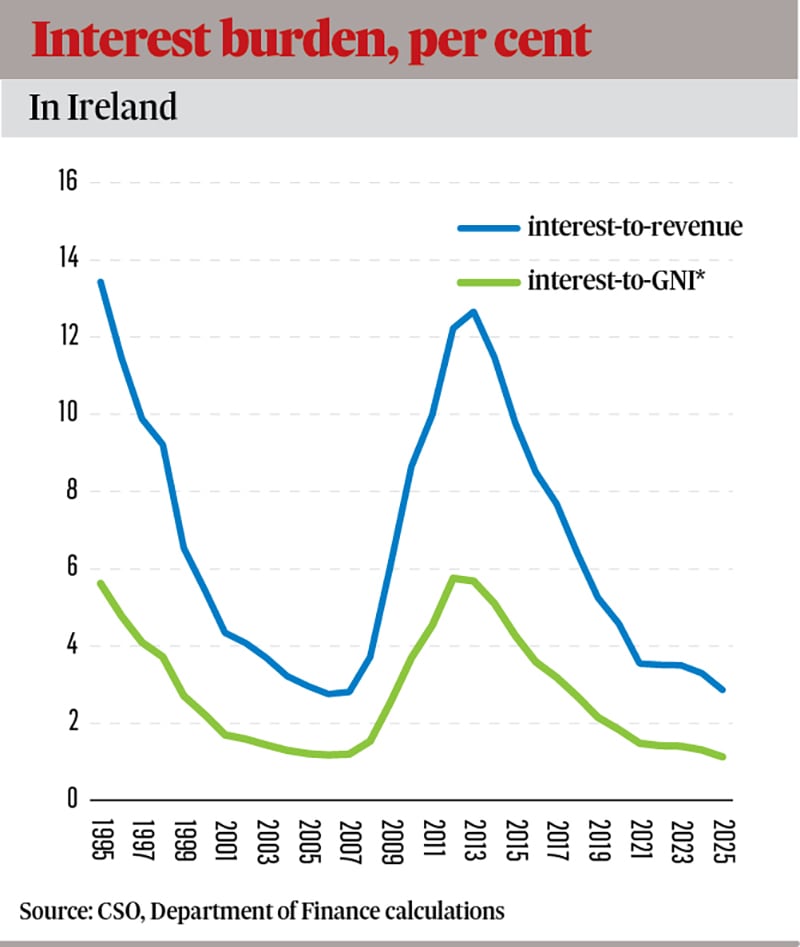

About €8 billion to €9 billion needs to be refinanced in both 2023 and 2024, but the total rises to a heftier €14 billion to €15 billion in each of 2025 and 2026

And trouble for European bond markets may not be far away. The ECB is promising to come forward with a new policy instrument to deal with market pressures on countries such as Italy, but this won’t be easy.

“The ECB has to thread the needle perfectly to avoid fragmentation in European bond markets,” according to economist Megan Greene, a senior fellow at the Harvard Kennedy School who points to the difficulties for the ECB in coming up with something which is of sufficient scale while not imposing overly onerous budget conditions. “I think its chances are very low,” she says. In other words, bond market pressures may lie ahead.

Ireland is not in the front-rank of exposed countries, she believes, due to a favourable schedule for debt repayments and recent strong growth. But “as a small, open economy, Ireland is vulnerable to an economic slowdown”, albeit not as exposed to immediate pressure as Italy and Spain.

Dermot’O’Leary, chief economist with Goodbody Stockbrokers, agrees the ECB is now facing a tricky choice in how to support states such as Italy, decisions which also have implications for Irish borrowing costs. The ECB can’t give an open guarantee to support peripheral countries, but any conditionality in terms of budget policy would be hugely sensitive. The risk is that the markets seek to test how far the ECB will go.

The NTMA has done pretty much all it can to prepare. It has extended out the repayments on Ireland’s debts as it refinanced in recent years, borrowing more than needed to avail of rock bottom rates. This has left it with a big pile of cash – in excess of €27 billion at the start of the year. To put this in context, Ireland borrowed almost €80 billion in the four years from 2018 to 2021. On the basis of existing forecasts for State borrowing, the total amount it reckons it needs to raise over the four years from 2022 to 2025 is less than half of this, at about €40 billion.

The amount of old debt which needs to be refinanced – including repayments on the 2010 bailouts to the EU funds – is, as Greene points out, relatively modest. There are two redemptions this year totaling €11.8 billion. About €8 billion to €9 billion needs to be refinanced in both 2023 and 2024, but the total rises to a heftier €14 billion to €15 billion in each of 2025 and 2026, counting in repayments to the EU. O’Leary of Goodbody points out that even at current higher interest rates, the price Ireland will pay for new borrowings over the next couple of years will be less than the rate on the debt being retired. “Debt sustainability will continue to improve,” he points out, provided borrowing rates don’t spike unexpectedly.

Ireland has had the wind behind it in terms of the national debt in recent years. Interest rates have been at rock bottom, the ECB has been buying heavily and the economy, bar a judder in early 2020, has grown remarkably strongly. Now, a lot of things are turning. Interest rates are on the rise, though they remain modest by historical standards. The ECB is withdrawing from new purchases of government debt. For now, forecasters expect the economy to continue to grow, albeit not as strongly as in recent years. But all acknowledge the uncertainty and the risks. This is the pinch point for Ireland – the risk of a recession largely sparked by external events, combined perhaps with a hit to corporate taxes.

This means Ireland’s financial management needs to be careful heading into the budget. It is a question of deciding what the right balance is between spending the resources available – while not fuelling inflation – and ensuring the public finances stay on the right path. Having an existing high debt level narrows the room for manoeuvre. So do the looming pressures on the public finances due to the long-term ageing of the population – which will start to really hit the deficit and debt numbers from around 2025.

If recession fears grow, bond markets in bigger countries such as the US could even benefit, as this would lower inflationary fears. But if this happens there will be a reckoning too – big countries such as the US will be safe havens for cash, but smaller ones will come under the spotlight. Investors will again be forensically looking at how each State is performing and assessing risk. Ireland needs to stay on the right side of the game to come.