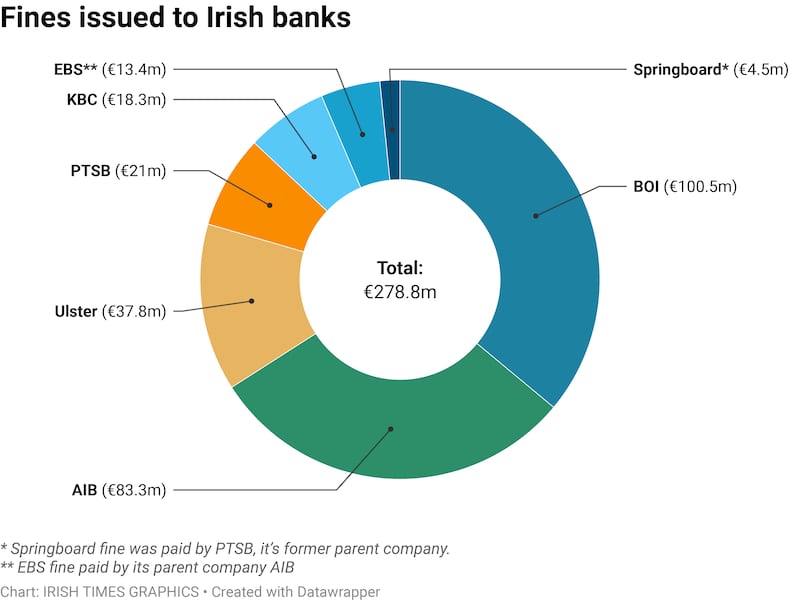

Bank of Ireland has been fined a record €100.5 million for its role in the State’s tracker mortgage scandal, which resulted in huge overcharging of borrowers and an industrywide loss of 327 homes.

The Bank of Ireland penalty eclipsed the previous record of €96.7 million levelled against AIB and its EBS subsidiary in June — and brings total tracker fines against seven lenders subjected to enforcement investigations to almost €279 million.

The Central Bank said Bank of Ireland’s failures resulted in the loss of 50 properties, including 25 family homes, which would have been avoided if it “had complied with the most basic fundamentals of its consumer protection obligations”.

Across the industry, property losses amounted to 327, of which 98 were family homes, according to figures contained in individual sanctions cases.

READ MORE

The Bank of Ireland fine is on top of the €186.4 million that it has already paid to 15,910 affected customers, who were identified before and as part of the Central Bank’s tracker mortgage examination.

Bank of Ireland admitted to 81 separate regulatory breaches as part of the regulatory investigation, covering a period between 2004 and June of this year in which customers were either denied their right to a cheaper mortgage that tracks the European Central Bank (ECB) interest rate or were put on the wrong rate.

The regulator found that Bank of Ireland, which stopped offering tracker loans at the height of the financial crisis in October 2008, had provided unclear documents to customers before then assessing their rights to a tracker rate after a fixed-rate period.

[ Analysis: Last tracker fine against an Irish bank does not bring saga to an endOpens in new window ]

Bank of Ireland repeatedly, over a period of over nine years, interpreted these unclear documents in its own favour and denied customers a tracker rate, it said. Even when it acknowledged the scale of wrongdoing, its initial refunds and compensation proposals fell short of supervisors’ expectations and “were indicative of a lack of understanding or consideration on its part of the impact that its failings had on its customers”.

As recently as June, some six fresh cases were identified for refunds and compensation, Central Bank officials told reporters on Thursday.

“Customers are entitled to expect that they will be treated fairly and that financial institutions will act in their best interests. Bank of Ireland failed to meet these most basic expectations for almost 16,000 of its customers over an extended period of time,” said Seána Cunningham, the Central Bank’s director of enforcement.

“Our investigation exposed a culture in Bank of Ireland which, when faced with a choice, prioritised its own interests with little to no regard for the impacts on its customers. There were a series of missed opportunities during which Bank of Ireland could have done the right thing by its tracker mortgage customers. Despite these opportunities, Bank of Ireland repeatedly interpreted unclear contractual terms in its own favour and against the customer, which continued the harm and loss caused to customers over many years.

While the regulator determined an appropriate fine for the bank to be €143.6 million, it reduced that by 30 per cent, in line with the standard discount applied to cases that are settled.

Permanent TSB (PTSB) and its former sub-prime unit Springboard Mortgages, KBC Bank Ireland and Ulster Bank had each been hit with penalties in recent years.

More than 41,000 borrowers were affected by the industrywide debacle, going back to 2008. Irish banks have set aside €1.5 billion of provisions in recent years in relation to the tracker scandal.

The tracker issue has so far cost Bank of Ireland almost €330 million since 2016 in refunds and compensation, legal fees and administrative expenses, and provisions set aside for a Central Bank fine.

The imminent closure of the Bank of Ireland case comes days after the Government announced last Friday that it had sold its remaining shares in the lender, making it the first to return fully to private ownership following the State’s crisis-era €64 billion rescue of the financial system.

Irish lenders stopped issuing tracker mortgages — where interest rates are typically set at a one percentage point premium to the European Central Bank’s main lending rate — in 2008 as their own funding costs jumped amid the global financial crisis.

While holders of tracker mortgages benefited as the reference ECB rate dropped from 3.75 per cent in late 2008 to zero in 2016 — and borrowers on other products faced higher charges — tracker loans have been automatically affected by the ECB’s recent rate hikes. The ECB has raised its main rate to 1.25 per cent since late July and is on track to increase borrowing costs further in the coming months.