The relentless rise in rents is continuing, according to the latest figures from the Residential Tenancies Board. The release of numbers from the third quarter of last year offers a complete analysis of all the data which the board collects from its work on new tenancies, as well as data on existing tenancies coming from the obligation for landlords to renew tenancy registrations introduced in 2022.

With rents doubling since their trough in 2013 and near the top of international league tables, there is no doubt the rental market and the wider ripples it causes are at the very centre of the housing crisis.

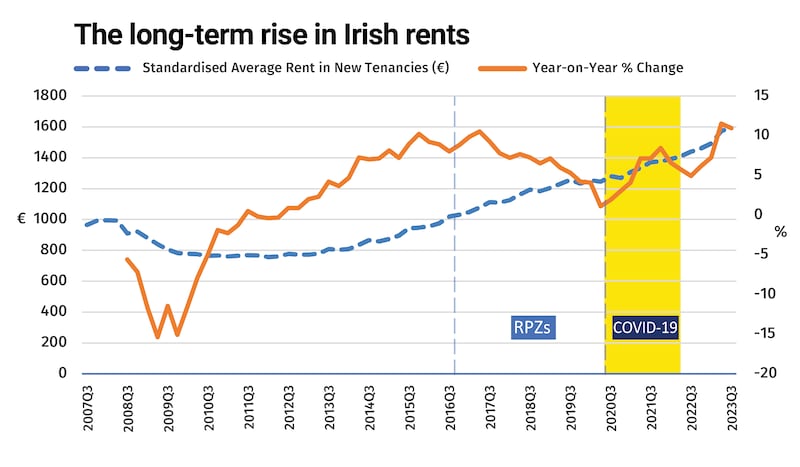

1. No end to rent increases

Rents are continuing to rise, even if the rate of increase is slowing. Bar a blip during Covid-19, the combination of a rising population and workforce and a chronic shortage of properties in many parts of the market have kept rents rising steadily. Looking at new tenancies, that national average rent climbed by 11 per cent year on year, well ahead of inflation of 5.1 per cent over the same period. The average rental in a new tenancy was just under €1,600 a month and over €2,100 in Dublin. In Cork the figure was €1,386.

Rental levels for new tenancies bottomed out in 2013 and have generally risen steadily since. Rents more or less stalled during the first lockdown – partly because many people working here returned to their home countries – but have surged as the economy reopened, with annual rates of increase remaining in double figures. The increase from €800 at the bottom of the market to more than €1,600 is striking, even if rental costs after the crash had fallen to abnormally low levels – they were around €1,000 a month before the crash hit.

Looking at quarterly trends, the rate of increase has been slowing on average nationally – with a 1.6 per cent rise in the last quarter. But a key message is that this is entirely due to a slowdown in Dublin, where the quarterly increase was 0.6 per cent. Outside Dublin city, the quarterly rise was 5.8 per cent and outside the Greater Dublin Area (GDA) it was 7.3 per cent. Rents remain lower outside the GDA, of course – €1,253 on average – so there may be an element of catch-up here.

Lack of supply in regional areas, part of an overall fall in the number of new registrations, is certainly a factor. There is no obvious pattern, the counties with the largest increase in annual rents on new tenancies being Wexford (23.5 per cent), Donegal (23.4 per cent), Clare (19.4 per cent), Roscommon (19.3 per cent) and Kilkenny (19.2 per cent). Conceivably, remote working may also be a factor, as some people give up on the Dublin market.

On the flip side, some increase in apartment availability in Dublin may have been a factor slowing the rise in rental costs in the capital.

2. New tenancies versus existing ones

The average rental level in existing tenancies, at €1,357, is close to 18 per cent lower than in new ones. In Dublin the figure for existing tenancies is €1,788. The index for existing tenancies is new, running just from the third quarter of 2022, but it provides useful information for policymakers. The annual increase in rental in existing tenancies is 5.2 per cent, showing how this part of the market is affected by rental pressure zones (RPZs), where annual increases are limited. The RTB warns that the fact that the 5.2 per cent annual rise is ahead of the 2 per cent RPZ annual limit does not necessarily indicate that landlords are breaching the rules. The RTB data covers the entire State – including both RPZ and non-RPZ areas – and it says that the data is also affected as some tenancies end and others are registered as existing tenancies for the first time. There is, in other words, what statisticians call a lot of “noise” in the figures. Nonetheless, they do raise the issue of compliance, and the RTB says it will use the data to investigate possible breaches of the rules. The average annual increase in rents in existing tenancies in Dublin – all of which is am RPZ – was 4.3 per cent.

3. Pressure points in the market

Affordability is an issue across most of the Irish rental market. Nearly one in three new tenancies now involves a rent of over €2,000 a month and one in every two in Dublin. Even as interest rates increase, Banking & Payments Federation Ireland figures show average mortgages for first-time buyers at roughly the time covered by the RPZ figures – at €1,139 for purchasers of an existing property and at €1,437 for those buying a new home – remain below rental levels.

While further mortgage rate rises will have pushed up repayments a bit in the meantime, mortgage repayments will remain below those of new tenancies across much of the State – though in some cases will have caught up with the average of existing tenancies.

Dublin remains the most obvious general pressure point in the market, with rents for new tenancies of over €2,000 on average, rising to €2,113 in Co Dublin and as high as €2,638 in Stillorgan in south Co Dublin, which is the highest in the State (it also has the highest figure for existing tenancies, at just over €2,400). For Dún Laoghaire/Rathdown the average for new tenancies is more than €2,400 a month. Rents in other cities also remain high, with Galway standing out at an average of close to €1,700. The figure for Cork is €1,500.

An interesting insight is the gap between the rise for existing tenancies in South Dublin at 3.6 per cent versus 20.4 per cent for new tenancies -reflecting, the RTB says, the new supply of apartments in that area.

The scramble for larger rental properties is also reflected in the figures, with average annual increases of 13 per cent and more for new tenancies in three- and four-bedroom houses. New tenancy rents for houses in Dublin rose by an annual 12.7 per cent, the highest annual growth rate recorded to date.

4. A lack of new supply

An ongoing story in the private rental market is a fall-off in supply. Estate agents have reported significantly more sales by landlords than new buy-to-rent purchases. And while new supply has come on the market – with an increase in apartments in Dublin in particular – many are expensive and overall availability is still low. Some 14,000 new tenancies were registered in quarter three of 2023, a 37.7 per cent fall from the same period in 2022. The RTB says some caution is needed here as late registrations may increase the 2023 number a bit. Nonetheless, it says this continues the trend of decline in new tenancy numbers and of reduced turnover in the private rented sector. It also said the normal seasonal surge in registrations due to students returning to college was not evidenced in 2023. Just over half of all new tenancies were in the Greater Dublin Area in quarter three and 78 per cent of these were for apartments. Together with the fall-off from last year, this suggests that new supply of houses for rental – and more generally of properties in many areas outside Dublin – remains very low.

5. An international outlier

While the RTB figures do not look at international comparisons, we know from recent Eurostat figures that Ireland is one of the most expensive markets to rent in Europe. Rents have doubled in Ireland since the crash, while across the EU the figure is around 22 per cent, and just 3 per cent over the past year. So the gap continues to grow. And while exact international comparisons are difficult because of the varying nature of markets, the apartments on offer and supports available to renters, rents in Dublin are now close to the top of the league of European cities and ahead of big centres such as Barcelona, Hamburg and Brussels. And, as we know, the chronic shortage of supply also means that many potential renters simply cannot find a property – or at least one they can afford. Meanwhile those who are renting are often paying too much of their income on rent – and so cannot afford to save to buy a house, or even spend to have a reasonable lifestyle.