The parties are about to launch their manifestos. And as their basis they will be using updated Department of Finance estimates for the public finances in the term of the next government. These predict that there will be €11 billion in "unallocated resources" in the next five budgets – on the face of it plenty to fund party promises. But "unallocated resources" does not mean money that whoever is finance minister will necessarily have to allocate on budget day to new spending projects or tax cuts. In particular, future public pay increases and other inflationary pressures are likely to eat up a lot of the cash. So the risk is that the parties are going to try to win our votes with promises funded by money which may not actually be there. This is not uncommon for an election campaign, but the parties can't do this and at the same time claim to be super prudent in their management of the public finances. Here are the things to watch.

1. The background

Budget 2020 was drawn up on the basis of the UK leaving the EU without a withdrawal deal at the end of this month. This now won’t happen. Because of this, the Department of Finance recalculated the budgetary outlook for this year and subsequent years on the basis of a more rosy scenario, which is that the EU and UK will conclude a trade deal and avoid a hard Brexit. Economic growth is expected to be 3.9 per cent this year, falling gradually to 2.5 per cent by 2025 – slower than the growth surge of recent years.

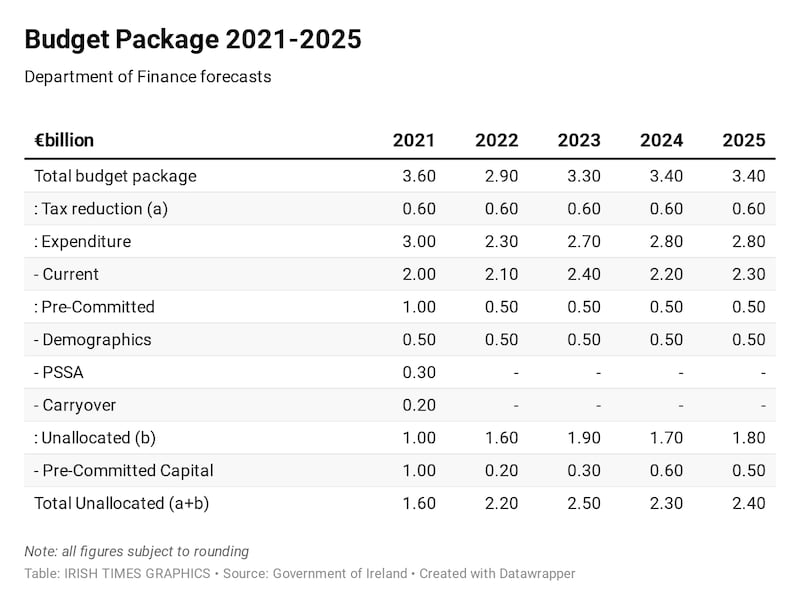

You can see from the table that the projections lead to the budget being in surplus. The PSSA referred to is the public sector stability agreement, the current pay deal. Money pencilled in for tax cuts and unallocated cash available for spending are added together to give a total for “unallocated resources”.

One obvious danger is that there is some hit to growth or tax revenues – either from a hard Brexit at the end of this year, or some other event. Some allowance is already made for a fall-off in corporation tax revenues from 2022 on due to international reforms, though judging the exposure here is very difficult. And there is €500 million allocated in additional annual contributions from 2021 on to a rainy day fund. So there is some resilience in the figures. But make no mistake, if the UK crashes out of the EU trading regime without a deal in December, the figures will have to be revised down sharply.

Part of the debate in the days ahead will – or should – be about what happens if the growth forecasts are not met, or corporation tax receipts fall even more rapidly than expected. Crucially, parties need to outline their priorities if this happens and they can’t afford all they promise. There will be trade-offs. And decisions to be made about whether the budget surplus should be run down and in what circumstances.

With national debt still elevated at around €200 billion, the State remains exposed, even if rock bottom international interest rates in recent years and the return of confidence in Ireland’s finances have delivered a huge boost through lower borrowing costs.

But there are other reasons for caution, too and other reasons to believe that rather than being able to afford to give a bit to everyone, the parties will have to make the trade-offs.

2. Spending pressures

Forecasts for future revenues and spending are, of necessity, surrounded with huge uncertainty, not only because economic growth may fall but also because budgeting is an imperfect science. In particular, it is vital in the debate that a realistic view is taken of what is – and is not – counted in the Department of Finance figures.

“Unallocated resources” do not equal the annual pot of money likely to be available to the minister on budget day for new spending commitments or tax cuts. Much of the money may be needed just to maintain current services in key areas such as health.

We know from past experience that pressure on spending is enormous – and in particular the figures as set out do not include an allowance for a successor to the current public sector pay agreement, which is certain to lead to significant extra costs. Nor do they count in the near-certainty of other inflationary pressures. These costs come in addition to the price of an ageing population, which is counted in to the figures, though in the past the budget watchdog, the Irish Fiscal Advisory Council (Ifac) has said it does not believe that the department has always allocated enough under this heading.

So the point is that the €11 billion will not necessarily be available to the future minister in terms of additional resources for new spending or tax cut plans. A lot of it might be needed to just keep services and investment at current levels. Of course the golden goose of higher corporation tax revenue could keep on laying. But it seems unwise to rely on that either.

3. The numbers

So how do we calculate the pluses and minuses? With great caution, of course. The latest estimates, as they are not a formal update, will not be examined by the Ifac, which does sign off on formal budget figures and updates sent to the EU. But one paragraph in its recent report, examining the estimates made as part of the October budget, seems pertinent.

It said: “The Government’s medium-term spending forecasts are more realistic than they have been recently. Yet, they still rely on arbitrary technical assumptions for spending rather than Government plans or assessments of demographic and inflationary pressures, and they do not include any public sector pay agreement beyond 2020.”

What might this mean in practice? There are so many pluses and minuses that it would be a mistake to be too definitive. The essence of Irish public finance management, as we have seen, is that things can turn on a sixpence – for better and for worse. With annual revenue and spending both exceeding €60 billion it only takes a small change in both to make things quickly look bad.

The most obvious issue is higher spending on public pay and because of other non-pay inflationary pressures. Earlier Ifac estimates were that these would cost €1.33 billion extra in 2021, another €1.52 billion in 2022 and more in subsequent years. The Ifac also estimated that demographic pressures would add €800 million a year to spending, compared to the €500 million pencilled in by the Department of Finance.

The bottom line is that a large part of the €11 billion could be eaten up by pay and inflation pressures – the cost of continuing to provide what we have, rather than the “new stuff” beloved of election manifestos.

In fairness, there may be some leeway on the other side of the figures too, while still staying within EU rules. The department data does appear to have taken a conservative enough approach on the size of future budgets, for example, and more leeway on spending may exist.

But the bottom line is still that what is actually left for new spending increases or tax cuts may still be well below the €11 billion figure.

4. What to ask the parties

We will have to see how this is dealt with in the party manifestos. But already the costly promises are spilling out – on housing, health, pensions and so on. The underlying point is that there will be cash to spend on key priorities, but whoever is in power will have to face choices, or trade-offs. Pushing more into health and housing may mean, as it has done in recent years, avoiding any cuts in the income tax burden, or cutting the planned increase in spending somewhere else. Agreeing another round of public pay rises will cost, too – and doing so is likely as private sector wages increase.

Improvements have been made in the way we budget and forecast the exchequer figures. Aiming for a surplus and a rainy day fund, while counting in a fall in corporate tax revenues, will give some room for manoeuvre. But we have seen in recent years how the seemingly relentless demands for spending add up.

The bottom line is it would be better to realise this, rather than pretending that a whole host of spending and tax plans will be paid for by economic growth.